Home Value Index up 0.8% in September as demand/supply imbalance continues to push values higher - CoreLogic

Contact

Oct 3, 2023

Home Value Index up 0.8% in September as demand/supply imbalance continues to push values higher - CoreLogic

Utilising a fresh model upgrade, CoreLogic’s national Home Value Index (HVI) recorded a 0.8% rise in September as the recovery trend moved through an eighth consecutive month of growth.

-

CoreLogic’s research director, Tim Lawless

CoreLogic’s research director, Tim Lawless

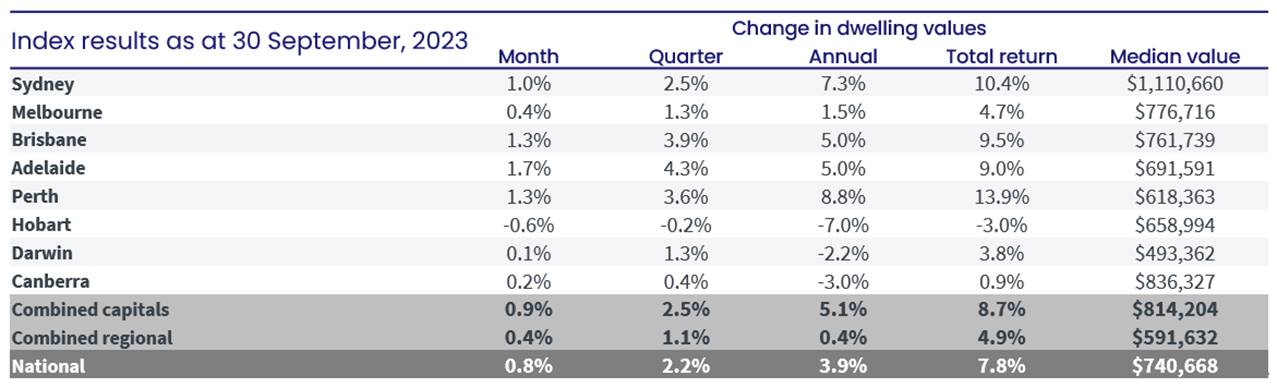

Utilising a fresh model upgrade, CoreLogic’s national Home Value Index (HVI) recorded a 0.8% rise in September as the recovery trend moved through an eighth consecutive month of growth. The rise follows a 0.7% lift in August (revised down from 0.8%) taking the quarterly pace of growth in national home values to 2.2%. Quarterly growth has eased from a 3.0% gain in the June quarter, reflecting a slowdown as advertised stock levels rise, helping to take some heat out of the market.

The September quarter saw Adelaide recording the highest capital gain at 4.3%, followed by Brisbane at 3.9% and Perth at 3.6%. At the other end of the growth spectrum is Hobart where values were down -0.2% over the quarter, taking the southern capital to a new cyclical low.

CoreLogic’s research director, Tim Lawless, noted the performance of the housing market in each city reflects the underlying supply dynamic. “The three capitals recording the highest capital gain each have advertised supply levels that are around 40% below their previous five-year average. Advertised supply levels across Hobart, where values are still trending lower, have been holding at above average levels since June last year and were almost 40% above its five-year average.”

Since finding a trough in January, the national index has recovered by 6.6%, however home values remain 1.3% below record highs recorded in April last year.

Tim Lawless noted at the current rate of growth, we are likely to see the national HVI recover to a new nominal high by the end of November.

“We have already seen dwelling values reach new record highs in Perth and Adelaide. Brisbane looks set to reach a new record high in October, with home values currently only 0.6% below their previous peak. Hobart and Canberra have the furthest to go before staging a nominal recovery, with dwelling values remaining 12.4% and 7.0% below their cyclical highs from last year.”

Delving into the detail, the upper quartile of the capital city housing market has led the slowdown in the pace of growth. After leading the recovery cycle, the premium housing sector might be losing some steam, with the quarterly rate of growth across upper quartile dwellings easing back to 2.3% while the lower quartile growth rate accelerated to 3.2%.

“This shift is partly attributable to the lower value capitals such as Perth and Adelaide recording a faster rate of growth, however even in these cities it is the lower quartile that has outperformed,” Mr Lawless said.

In the more expensive cities, Sydney and Melbourne, the broad middle of the market is now recording the highest growth rate after previously being led by the upper quartile.

“Possibly we are starting to see renewed affordability challenges deflecting more demand towards the middle of the market where barriers to entry are lower,” Mr Lawless said.

Regional markets are continuing to lag the capitals with every ‘rest of state’ region recording weaker growth conditions relative to their capital city counterpart over the September quarter. At a broad level, the combined regional markets recorded a 1.1% rise in dwelling values through the September quarter which was less than half the gain across the combined capital city market (2.5%).

“Softer housing conditions across regional Australia looks to be more demand-driven, with the estimated number of home sales 6.5% lower than a year ago and 9.2% lower relative to the previous five-year average,” Mr Lawless said.

“In contrast, the estimated volume of home sales across the combined capital cities was 1.9% higher than a year ago and 6.3% above the five-year average.”

Most regional markets are also showing relatively low advertised supply levels which has been enough to place some upwards pressure on values. However, regional Victoria and regional Tasmania are exceptions, where advertised supply is above average and housing values trended lower over the quarter.

Contact Details:

Contact details:

Tim Lawless

Director of Research, CoreLogic

Email

47989

41448

Tim Lawless