Rate of decline in housing values eases in September - CoreLogic

Contact

Oct 3, 2022

Rate of decline in housing values eases in September - CoreLogic

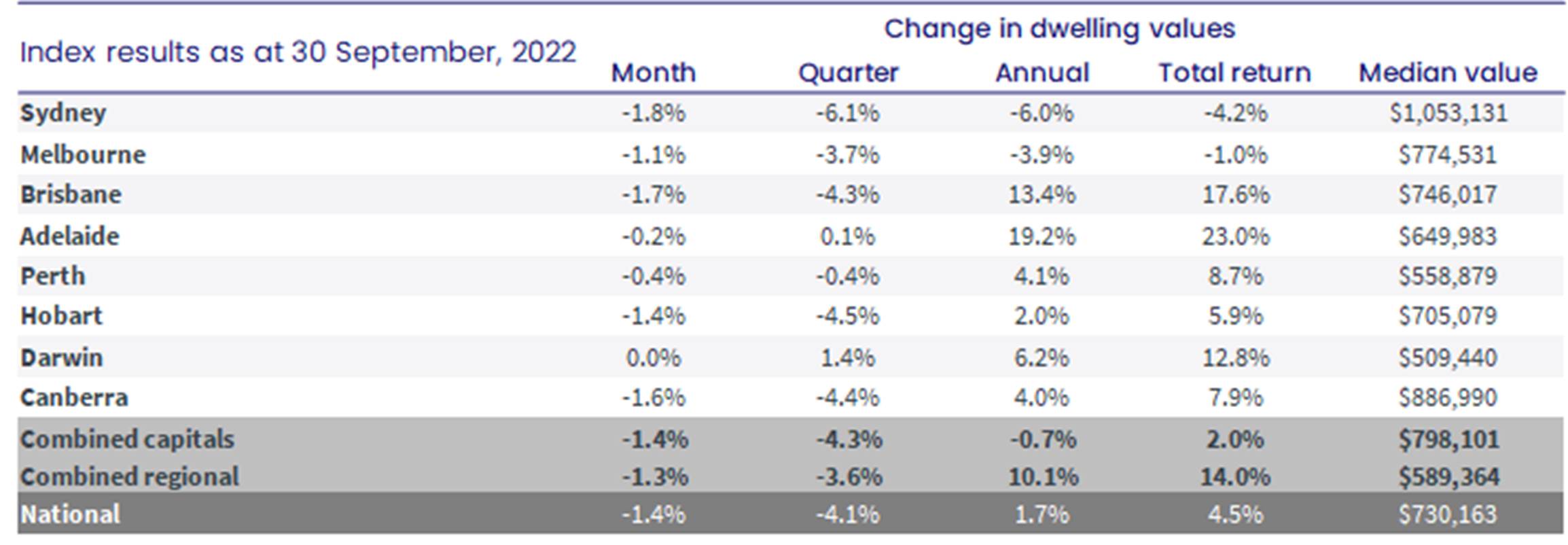

CoreLogic reported a further fall in housing values through the first month of spring, with the national Home Value Index (HVI) recording a -1.4% decline in September. Although values continue to trend lower, the rate of decline eased from a -1.6% fall in August.

-

CoreLogic’s research director, Tim Lawless.

CoreLogic’s research director, Tim Lawless.

The loss of momentum in the pace of value decline was evident across most of the capital cities and broad rest-of-state regions, with a few exceptions. Housing value falls accelerated in Adelaide and Perth this month, however both cities continue to record only a mild reduction in values relative to the other capitals (down -0.2% and -0.4% respectively in September). Sydney’s monthly rate of decline eased from -2.3% in August to -1.8% in September, Melbourne tapered from -1.2% to -1.1% and Brisbane falls went from -1.8% to -1.7%. Darwin remains the only capital city where housing values haven’t started to trend lower, although dwelling values remain -10.1% below the 2014 peak.

According to CoreLogic’s research director, Tim Lawless, it is probably too early to suggest the housing market has moved through the worst of the downturn. “It’s possible we have seen the initial shock of a rapid rise in interest rates pass through the market and most borrowers and prospective home buyers have now ‘priced in’ further rate hikes. However, if interest rates continue to rise as rapidly as they have since May, we could see the rate of decline in housing values accelerate once again.”

The reduction in the rate of decline came alongside an improvement in other indicators. “Auction clearance rates also trended upwards, albeit subtly, in September and consumer sentiment nudged a little higher as well on the back of strong labour market conditions,” Mr Lawless said. “We’ve also seen the flow of fresh listings continue to slide through the first month of spring, which is uncommon for this time of the year.”

After rising 25.5% over the recent growth cycle, housing values across the combined capitals index are now -5.5% below the recent peak, or in dollar terms, down approximately -$46,100. The combined regionals index, which recorded stronger growth conditions through the upswing (41.6%), peaked two months later than the capital cities (June 2022), with values down -3.6% through to the end of September (approximately -$21,700).

Although the rate of decline eased in September, Sydney continues to record the largest falls, with housing values now -9.0% or -$104,300 below the city’s January 2022 peak. After a later peak and subsequent start to its slide, Brisbane has almost caught up with Sydney’s monthly rate of decline, to be -4.3% / -$33,600 below its June 2022 peak.

Most cities continue to see a substantial buffer between current housing values and where they were at the onset of COVID in March 2020. At the combined capital city level, housing values would need to fall a further -13.5% before wiping out the gains of the recent growth cycle, while Melbourne, which saw a softer upswing than other regions (+17.3% from trough to peak), would only need to see a -4.3% fall in values before returning to pre-COVID levels.

Across the 307 SA3 sub-regions analysed nationally (excluding areas with low sales or low confidence scores), only 25 regions remained at record highs at the end of September.

“We are still seeing some resilience to value falls around the more affordable areas of Adelaide and Perth, as well as some regional markets associated with agriculture, mining and tourism,” Mr Lawless said.

The largest cumulative falls have been concentrated in areas of Sydney’s Northern Beaches, including the SA3’s of Warringah, Pittwater and Manly where housing values are down at least -14.5% since moving through a peak in early 2022, as well as flood affected areas across Richmond - Tweed.

“These areas saw housing values rise between 38% and 62% through the growth cycle, so most home owners are still well ahead in terms of equity in their home,” Mr Lawless said.

Contact Details:

Contact details:

Tim Lawless

Director of Research, CoreLogic

Email

46495

41448

Tim Lawless