Rising interest rates will be the smallest shock of the past two years - HIA

Contact

Aug 18, 2022

Rising interest rates will be the smallest shock of the past two years - HIA

“The rise in the cash rate will have a minor impact compared to the events of the past two years,” stated HIA Chief Economist, Tim Reardon.

-

HIAHIA Chief Economist, Tim Reardon.

HIAHIA Chief Economist, Tim Reardon.

“The rise in the cash rate will have a minor impact compared to the events of the past two years,” stated HIA Chief Economist, Tim Reardon.

HIA released its economic and industry Outlook Report for Australia today. The Outlook Report includes updated forecasts for new home building and renovations activity nationally and for each of the eight states and territories.

“The fastest increase in the cash rate in almost 30 years will bring Australia’s home building boom to an end, but there is a significant buffer of building work to be completed,” added Mr Reardon.

“The increase in interest rates to date has caused uncertainty for households, but it is well within their capacity to absorb. When the cash rate stabilises, confidence in the established and new home market will be restored quickly.

“In the detached market, key leading indicators reported by builders have weakened since the first increase in the cash rate and resulted in a sharp fall in new home sales in July.

“The cost of building a new home has increased significantly over the past two years and was starting to limit demand for new homes. Rising interest rates will accelerate this slowdown.

“Despite a slowing in sales, there remains a record volume of work on the ground and a near record volume of projects still to commence construction.

“Material constraints that have plagued builders for the past two years are starting to ease and this will see the cash flow problems experienced by builders passed up the supply chain as the ‘bull whip effect’ plays out. The acute shortage of land will be a major constraint on building in 2023 and labour constraints are persistent.

“The uncertainty around how far the RBA needs to increase interest rates to restore inflation back to its target range has impaired consumer confidence.

“Already the short-term international factors that initiated the inflationary spike are showing signs of improvement. Reduced shipping costs and times have assisted the volume of exports and imports. Weakening demand is also emerging as interest rates rise across major economies.

“Despite the uncertainty around the cash rate, demand for new homes – especially multi-units – will be supported by low unemployment, booming export markets, an acute shortage of rental homes and a return of overseas migrants, students and tourists,” concluded Mr Reardon.

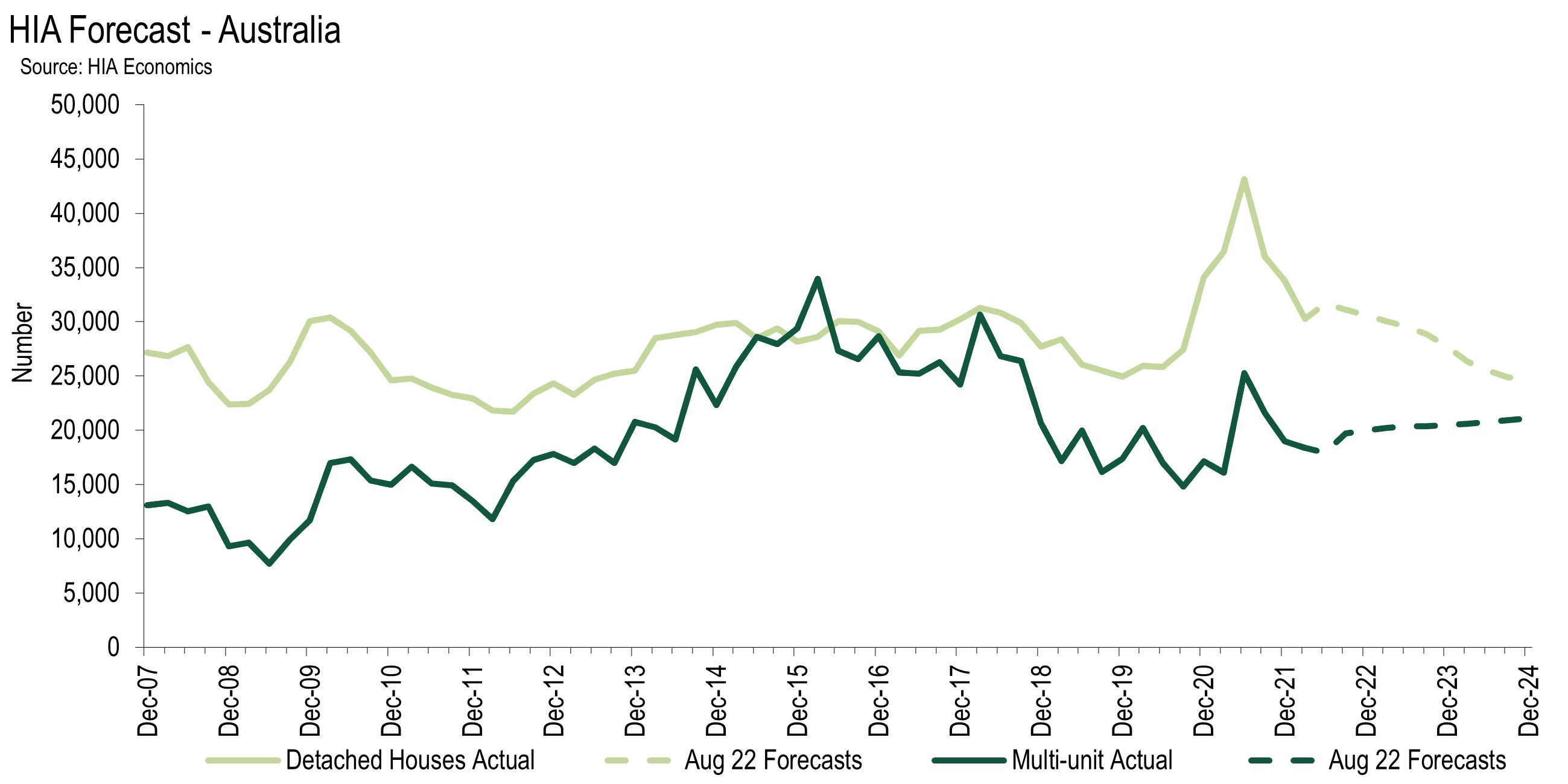

It is anticipated there will have been 131,730 detached starts in 2021/22. This is just 6.7 per cent below last year’s record. Unfortunately, the slowdown in starts will continue with 121,320 starts expected in 2022/23 through to a trough in 2024/25 of around 99,330 starts. Multi-unit starts will have been just 76,930 starts in 2021/22, up 4.8 per cent off the previous financial year, but 35.1 below the peak in 2015/16. Multi-unit starts are expected to increase by 4.4 per cent to 80,270 in 2022/23 with a further 2.5 per cent increase in 2023/24.

Contact Details:

Contact details:

Tim Reardon

Chief Economist, HIA

+61423 141 031

Email

46316

39867

Tim Reardon