Residential yields outperform compared to commercial assets

Contact

Jun 25, 2024

Residential yields outperform compared to commercial assets

By Vanessa Rader, Head of Research, Ray White Group.

-

Ray WhiteVanessa Rader Ray White

Ray WhiteVanessa Rader Ray White

The COVID-19 pandemic initially brought mixed results to the property market. Economic uncertainty led many to postpone property-related decisions, causing declines in residential values and a slowdown in commercial investment across all asset classes.

However, falling interest rates quickly stimulated activity, making 2021 the most active year on record for commercial investment.

A growing pool of buyers sought to diversify their portfolios, increasing demand for higher-yielding assets such as industrial units, retail shops, childcare facilities, and service stations.

With the cash rate reduced to 0.1 per cent and available financing, investment yields across all price points in the commercial market saw a swift reduction.

Institutional and offshore buyers purchased CBD office buildings and industrial asset portfolios at sub-4 per cent yields, while smaller, higher-risk assets often attracted private investors including first time buyers at staggering sub-5 percent yields.

As interest rates rose, sentiment towards these assets changed. While activity remained strong through 2022, 2023 saw a sharp decline in transactions as the increasing costs and limited availability of finance required higher investment yields.

Many owners faced distress as the cash rate increased by 425 basis points, with rental growth failing to keep pace with the rising cost of finance.

Despite rising finance costs, yields across all asset classes increased only slightly, not aligning with the rate hikes. For many assets, although capital returns declined, ongoing rental growth or stability kept total returns attractive enough to maintain tight yields.

The residential market, however, experienced a different trajectory during this period. After initial declines in house and unit values nationwide, low interest rates stimulated activity, pushing median prices to new highs, surpassing previous records.

The residential sector's recovery was driven by unique fundamentals. Australia's growing population, combined with the halt in construction activity during the pandemic and high costs of construction and labour, led to a persistent shortfall in housing supply.

This shortage put upward pressure on both values and rents. Commercial markets largely didn't experience these same pressures, with one notable exception being industrial.

This sector saw robust growth in space requirements during the pandemic, coupled with limited new construction due to land constraints. As a result, industrial properties continued to experience rent increases.

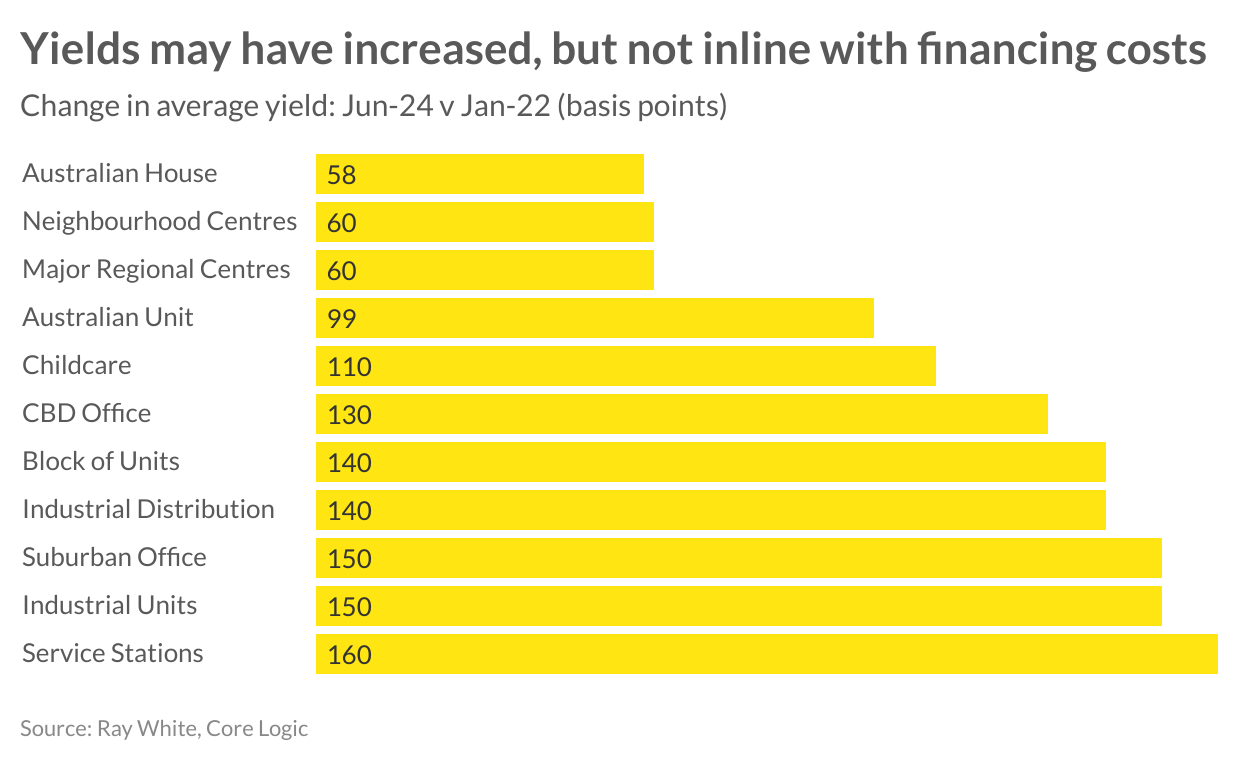

Australian residential property investment yields have remained closely aligned with the peak rates of late 2021 and early 2022.

House yields have only increased by 58 basis points over the last 2.5 years, despite growing difficulties in obtaining finance and higher interest rates. Unit yields have also performed well, rising by just 99 basis points.

Among commercial sectors, retail has emerged as the clear performer. After a decade of challenges, strong population growth has led to ongoing increases in retail trade, driving continued demand for space.

However, performance varies by asset type and location, with food and supermarket anchored assets like neighbourhood centres seeing only a 60 basis point change, similar to larger major regional centres that have recorded limited trading.

Industrial assets remain in high demand due to low vacancy rates in many regions and high construction costs, making existing built structures more attractive.

Larger assets that previously had unsustainably low yields have seen increases of around 1.4 percentage points, while industrial units with broader appeal have experienced yield increases of approximately 1.5 percentage points on average across the country.

The office sector continues to face challenges post-COVID due to work-from-home pressures, resulting in high vacancy rates and pressure on returns with high incentives across all CBDs.

Limited transactions have capped current reported yields, although anecdotal evidence suggests actual yields may be much higher.

CBD yield growth over this period is officially up 130 basis points, but could be as high as 250 basis points. Suburban offices show similar results.

The alternative sectors have shown mixed results. Their low barrier to entry, due to affordable prices, initially attracted many private and first time investors, significantly lowering yields.

Assets such as childcare facilities, service stations, and blocks of units have seen yield increases, but these can vary considerably based on factors like location and quality.

Encouragingly for asset owners, the 425 basis point increase in interest rates has not translated to a proportional growth in investment yields.

Although values have declined for most commercial assets, yields have remained relatively stable due to limited stock in the market.

While holding costs have risen, the absence of widespread distress has kept yields in check with many owners now looking towards potential interest rate reductions to aid in continued price corrections.

Related reading:

Data centres: the next big commercial alternative asset class - RWC

Contact Details:

Contact details:

Vanessa Rader

Head of Research, Ray White Group

0432 652 115

Email

48565

48564

Vanessa Rader