Australia's smallest cities drive growth in national housing values as Sydney and Melbourne decline - CoreLogic

Contact

Apr 1, 2022

Australia's smallest cities drive growth in national housing values as Sydney and Melbourne decline - CoreLogic

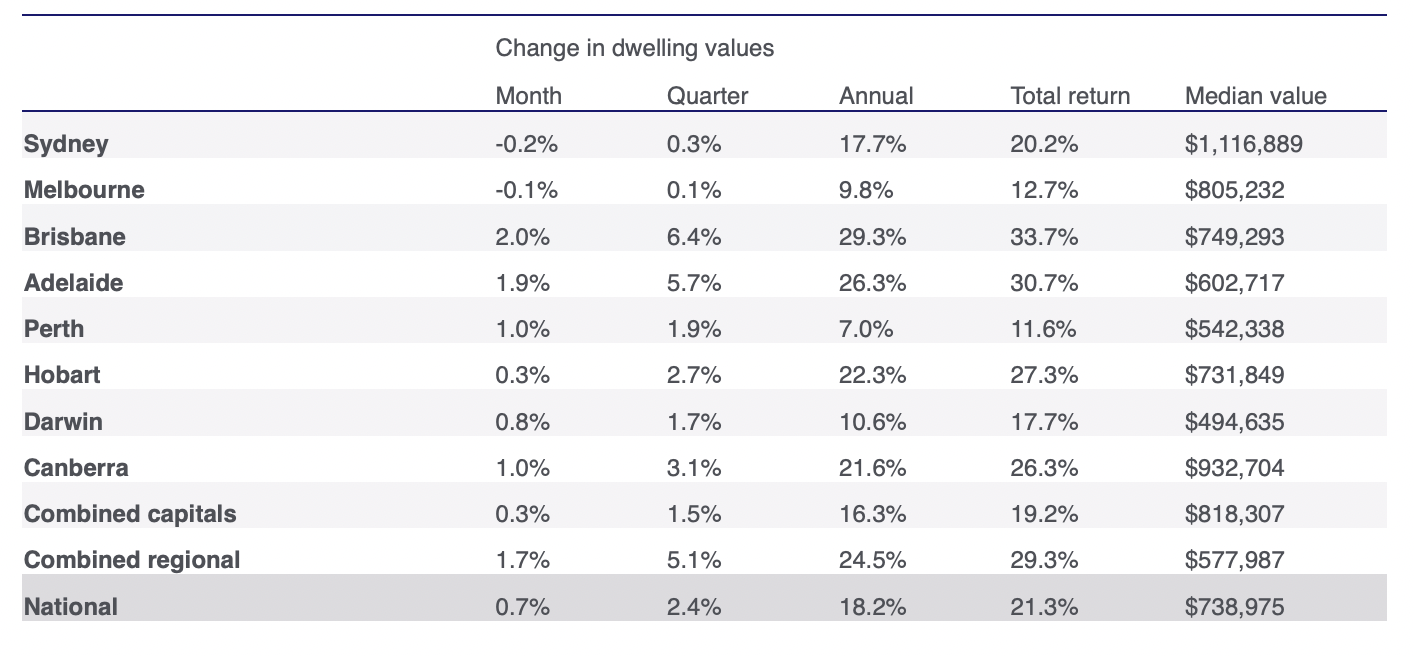

CoreLogic’s national Home Value Index (HVI) was up 0.7% in March, a subtle increase on the 0.6% lift recorded in February. The uptick in the monthly rate of growth was primarily driven by stronger conditions in Brisbane, Adelaide, Perth and the ACT, along with several regional areas, offsetting a slip in values across Sydney and Melbourne.

-

Tim Lawless, Head of Research, CoreLogic.

Tim Lawless, Head of Research, CoreLogic.

CoreLogic’s national Home Value Index (HVI) was up 0.7% in March, a subtle increase on the 0.6% lift recorded in February. The uptick in the monthly rate of growth was primarily driven by stronger conditions in Brisbane, Adelaide, Perth and the ACT, along with several regional areas, offsetting a slip in values across Sydney and Melbourne.

The first quarter of the year has seen Australian dwelling values rise by 2.4%, adding approximately $17,000 to the value of an Australian dwelling. A year ago, values were rising at more than double the current pace, up 5.8% over the three months to March 2021 before the quarterly rate of growth peaked at 7.0% over the three months ending May 2021.

Sydney’s growth rate is showing the most significant slowdown, falling from a peak of 9.3% in the three months to May 2021, to 0.3% in the first quarter of 2022. Melbourne’s housing market has seen the quarterly rate of growth slow from 5.8% in April last year to just 0.1% over the past three months.

CoreLogic’s research director, Tim Lawless, says while the monthly rate of growth was up among some cities and regions, there is mounting evidence that housing growth rates are losing momentum.

“Virtually every capital city and major rest-of-state region has moved through a peak in the trend rate of growth some time last year or earlier this year,” Mr Lawless said.

“The sharpest slowdown has been in Sydney, where housing prices are the most unaffordable, advertised supply is trending higher and sales activity is down over the year.

“There are a few exceptions to the slowdown, with regional South Australia recording a new cyclical high over the March quarter and some momentum is returning to the Perth market where the rate of growth is once again trending higher since WA re-opened its borders.”

With the softening in market conditions, the national annual growth rate (18.2%) has fallen below the 20% mark for the first time since August last year, after reaching a cyclical high of 22.4% in January 2021.

Mr Lawless said the annual growth trend will fall sharply in the coming months, as the strong gains recorded in early 2021 drop out of the 12-month calculation.

National housing turnover is also easing, with preliminary transaction estimates for the March quarter tracking 14.3% lower than the same period in 2021, but still 12.2% above the previous five-year average.

“Nationally, the volume of housing sales is coming off record highs but there is some diversity across the capital cities in these figures as well. Our estimate of sales activity through the March quarter is 39% lower than a year ago in Sydney and 27% lower in Melbourne, while stronger markets like Brisbane and Adelaide have recorded a rise in sales over the same period.”

Regional Australia continues to show some resilience to a slowdown with housing values across the combined regional areas rising at more than three times the pace of the combined capital cities through the March quarter. Regional dwelling values increased 5.1% in the three months to March, compared with the 1.5% increase recorded across the combined capital cities. The rolling quarterly growth rate in regional dwelling values has consistently held above the 5% mark since February 2021.

Australian Bureau of Statistics (ABS) regional population growth figures for FY2020-21 help explain the strong housing conditions outside of the capitals. The number of people living in regional areas of Australia increased by almost 71,000 residents, while residents living in the capitals fell by approximately 26,000 (mostly due to a sharp drop in Melbourne and, to a lesser extent, Sydney.

Index results as at 31 March, 2022

Contact Details:

Contact details:

Tim Lawless

Director of Research, CoreLogic

Email

45715

41448

Tim Lawless